For Your Benefit: How will the WEP & GPO Repeal Affect Connecticut Teachers?

Many retirees—approximately 2.8 million, potentially including you—are eagerly awaiting the benefits of the recently signed Social Security Fairness Act, enacted on January 5, 2025. This landmark legislation primarily repeals two provisions:

The Windfall Elimination Provision (WEP)

The Government Pension Offset (GPO)

Both of these provisions had a significant impact on the Social Security benefits of state and municipal government employees, police officers, firefighters, railroad retirement system participants, most permanent federal employees hired before 1984, self-employed individuals with low net earnings, and most specifically to this blog post public school teachers, including those in Connecticut. The new law repeal is set to restore full benefits to those affected by these laws, retroactive to January 2024.

—While this is an exciting turn for many retirees, it is important to note that the Social Security Administration (SSA) has stated that it may take a year or more to fully restore the benefits due to the complexity of recalculating payments for millions of affected individuals.—

For many who are affected by this new legislation but don’t have time to research the matter themselves, the main questions are likely:

“What does this all mean?” and

“How much will this affect my monthly benefit?”

In this article, I’ll explain what the WEP and GPO were, highlight key components of the new legislation, and discuss how the repeal can positively impact your Social Security benefits—whether you're collecting your own benefit, a spousal benefit, or a survivor's benefit.

How Did The Windfall Elimination Provision Affect Me?

For decades, this law has been in effect, initially signed by President Reagan on April 21st, 1983. The initial idea behind this law, whether right or wrong, was to prevent the disproportionate collection of retirement benefits by state or municipal employees who became eligible to collect both a non-covered pension and Social Security benefits.

Prime example: Think of our loved Connecticut public school teachers, police officer, firefighter, or some variation of a state/municipal employee who worked 20 years at that career and became eligible to collect from a non-covered pension (a plan in which Social Security taxes were not withheld). Then, they went on to work 10 years in a second career where they paid Social Security taxes for the required minimum 40 quarters, making them eligible to collect Social Security.

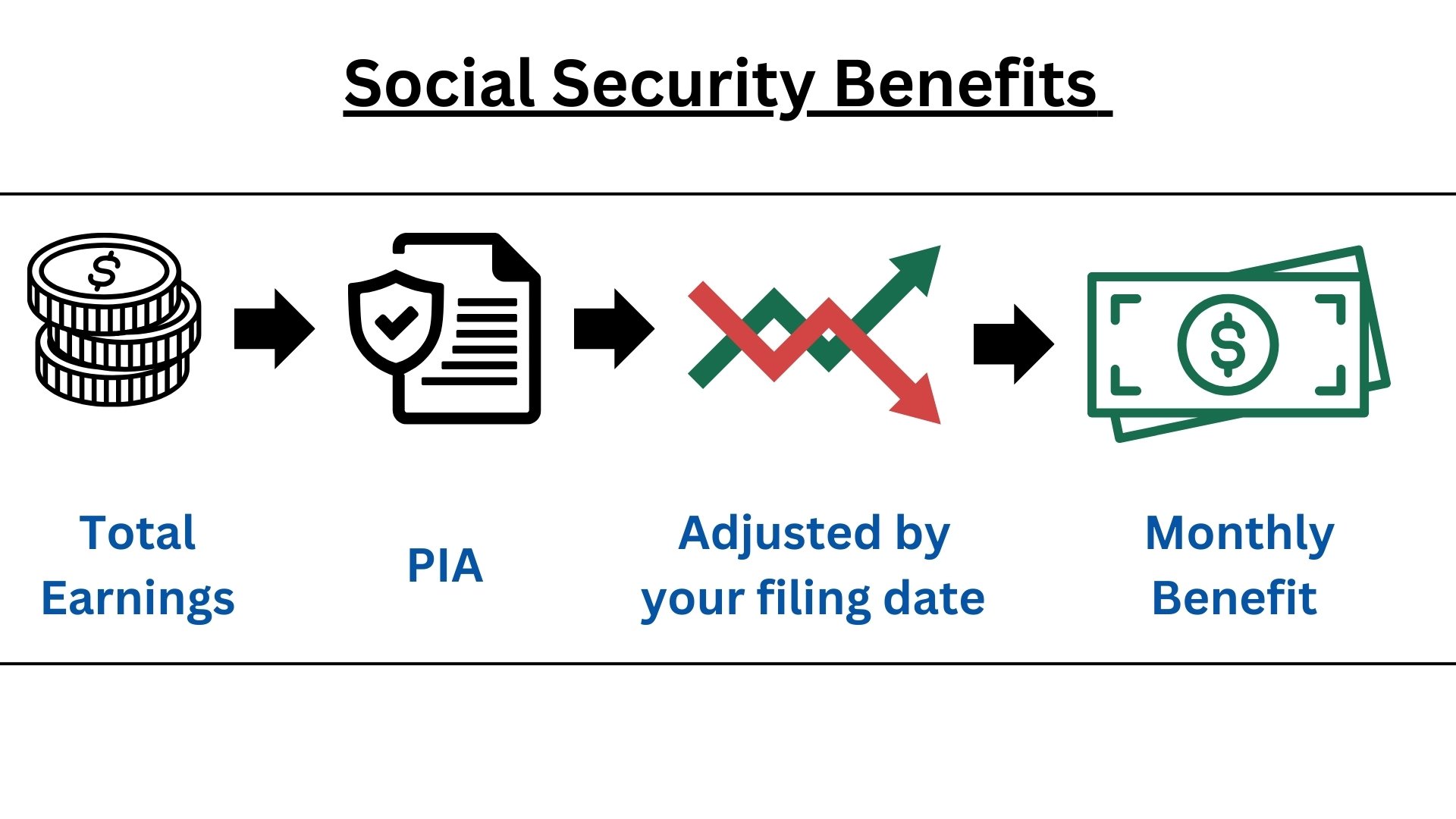

People in this situation faced a significant reduction in their monthly Social Security benefit through the WEP reduction. To properly explain how this affected the benefit received, I need to provide a brief overview of AIME and Social Security bend points.

The AIME (Average Indexed Monthly Earnings) is used to calculate your PIA (Primary Insurance Amount), which in turn is used to determine your monthly Social Security benefit. The AIME is calculated by taking the sum of the highest 35 years of earnings in your employment history and dividing that number by 420 (the number of months in 35 years).

Once we have the AIME, we must reference the Social Security "Benefit Formula Bend Points" chart. This chart is used to determine the first and second bend points for calculating your PIA, specifically in the year you turn 62. This may seem complicated, but once you understand the process, it really is quite simple.

For example: Let’s assume Samantha spent 20 years working as a Connecticut school teacher, paying into her non-covered pension, and then started a second career later in life, where she spent 10 years (40 quarters) paying into Social Security. Samantha would now be eligible to collect her non-covered pension benefit, as well as Social Security.

Let’s assume her AIME was calculated to be $7,500. To determine her PIA (Primary Insurance Amount), we will reference the Benefit Formula Bend Points chart to see what the two bend points are for the year she turns 62 — let’s assume that was in the year 2022.

Now with the associated bend points that correspond with the year Samantha will turn 62 (reference the charge above) we can calculate her PIA.

For reference: for those employed by a company that has withheld taxes to be paid in to Social Security ONLY, the following is how their PIA would be calculated using the mentioned bend points:

Every dollar earned up until the first bend point is accounted for at 90%

(In this case, up to $1,024).Every dollar earned between the first and second bend points is accounted for at 32%

(In this instance, every dollar between $1,024 and $6,172).Every dollar earned beyond the second bend point is accounted for at 15%

(In this case, every dollar beyond $6,172).

So, for that individual, with a generated AIME of $7,500, their PIA would calculate to:

90% of $1,024 ($921.60)

32% of $5,148 ($1,647.36)

15% of $1,328 ($199.20)

For a combined total of $2,768.16, making up their entire PIA. Now, this is not the exact amount you will receive for your Social Security benefit, as other factors come into play, such as whether you elect to begin collecting your benefits immediately at 62, which will result in a reduction from your PIA amount. If you wait until your FRA (Full Retirement Age), this would be the expected benefit received. Or if you elect to wait to collect beyond your full retirement age, this will result in deferred retirement credits increasing your total benefit. But this is a side note from the point I’d like to discuss today, which we can go into more detail on in a later blog.

Back to our example of Samantha: Because Samantha would be collecting a benefit from her non-covered pension as well as Social Security, the previous legislation was in place to ensure that a disproportionate amount of retirement benefits wasn’t being collected. Again, whether this was right or wrong, let’s look at how her Social Security benefit would be affected by this WEP reduction.

Assuming Samantha has an AIME of $7,500, we will input her earned income just as we did in the previous example. The key difference is on the earned income up until the first bend point. Where previously I showed you it was accounted for at 90%, it will instead be accounted for at only 40%. Let’s look at the math:

40% of $1,024 ($409.60)

32% of $5,148 ($1,647.36)

15% of $1,328 ($199.20)

For a combined total of $2,256.16, making up her PIA. A total reduction of $512.00 to Samantha’s monthly Social Security benefit. Again, this amount would be subject to change depending on the factors we discussed above. However, this is a considerable amount of income lost for Samantha in retirement.

There are two caveats to this reduction:

The total reduction amount, in this case, $512.60, cannot exceed 50% of the pension benefit Samantha is receiving. So, if Samantha was receiving, let’s say, $800 monthly from her pension, the maximum her Social Security benefit could be reduced would be $400.

Secondly, the SSA(Social Security Administration) does recognize individuals who, despite having a non-covered pension, contributed Social Security taxes on over 20 years of “substantial earnings” in their alternate career where social security was paid in to. In this case for every year beyond the 20th year, the inclusion rate of the first bend point will be increased by 5%. So let’s say Samantha had reported 22 years of substantial earnings. Instead of the first $1,024 of her AIME being counted at 40%, it would rather be counted at 50%. This rule applies for every year beyond 20, until the inclusion rate is restored back to the original 90%. ( It cannot go beyond this number, even if more years of substantial earnings were included.)

Per the Social Security Fairness Act, signed into law this past January, this reduction will no longer be in effect, and benefits will be fully restored retroactive to January of 2024. Now, the SSA is currently doing their due diligence to determine when they will fully restore the benefits of those affected. Though it is unclear as to when this lump-sum payment of missed benefits will be satisfied, the SSA has signaled that it may take a year or more to recalculate and process payments to the millions affected. However, they anticipate you will be made whole in the relatively near future.

Just The Tip Of The Iceberg

I’d say this is a very good start and a good amount of relief for the currently affected retirees. But now we must discuss the second, and potentially much more impactful repeal cited in the new act. This would be the repeal of the Government Pension Offset (GPO). This law affected the treatment of spousal and survivor benefits under Social Security for individuals who were receiving pensions from government jobs not covered by Social Security. Again, this topic may be quite complex, but I will do my best to simplify exactly what was happening in these instances and share with you how the repeal of this law could significantly affect the retirement benefits you’re entitled to collect. This affects every individual differently, given their personal situations, which makes it very apparent the importance of interviewing and finding a financial advisor you can trust to assess your exact situation and paint a clear picture of how this all is or will affect your retirement income and help to create a sound retirement plan to provide you with the peace of mind you deserve.

As a sidebar, and in light of that thought, my name is Ryan Morrissey, CFP®, CLU®, CHFC®, CMFC®. I am the owner and principal wealth advisor of Morrissey Wealth Management. I’ve spent over 24 years in the financial industry guiding my clients to and through a successful retirement. The aim at my firm is to provide you with invaluable investment advice specific to your situation and needs, parlayed with comprehensive tax, Social Security, and Medicare planning. Put simply, we want to prepare you for a successful retirement, and once we get you there, provide the guidance you will need to ensure it lasts!

It’s important to note, we are a fee-only advisory firm, meaning myself and all our services are available to you with no added costs beyond the fee we will discuss. If you have been considering hiring a financial advisor to get started working on your retirement plan, or would like a second opinion on the one you currently have — I urge you to click the image below to view my availability and set up a free consultation at your leisure. I greatly look forward to speaking with you!

Now Back To The GPO Repeal

This is where we will see the greatest impact for retirees. The Government Pension Offset (GPO) was first signed into law by President Jimmy Carter in 1977. This law, again whether right or wrong, was created to prevent the “double dipping” of spousal and survivor benefits from Social Security for individuals who worked in a government/public position not covered by Social Security and collected a pension. Our example of the Connecticut public school teacher would be among this group. To simplify how the math worked out and explain how it will substantially affect the retirement benefits for the millions impacted, I will provide some examples of different scenarios to paint a clearer picture. However, the main element of the rule was that any individual aiming to collect a spousal or survivor benefit could only collect the portion of their calculated benefit that exceeded 2/3 of their government pension. This had a substantial impact on the benefit many spouses and survivors were able to collect, and in many cases, it eliminated their benefit entirely. Before we can go into some examples of how this will play out, we must first understand the difference between how a survivor's benefit and spousal benefit are calculated. This part can get rather complex, but I will aim to simplify and provide a brief overview of these calculations.

Calculating Your Spousal Benefit

I’ve created a few graphics for the next few parts we will discuss to depict the over arching idea of how the benefits are calculated.

As we previously discussed this is the line of calculations used to determine the social security benefit for an individual who has paid into social security for at least 10 years(40 quarters)

While there are many factors that come in to play to determine what your actual spousal benefit will be— This amount collected or eligible to be collected will be used to determine the amount of benefit owed for an individual’s spousal benefit.

A spousal benefit, is calculated as 50% of the PIA calculated for the spouse that did work at a social security covered job. Which can then be reduced if the spouse files for spousal benefits prior of their own FRA (unless they have a child in their care under the age of 16 or disabled).

Calculating Your Survivor’s Benefit

In the case of widows and widowers of deceased earners, it gets even stickier. A major consideration that will affect the monthly benefit received is whether the deceased earner, the surviving spouse, or both spouses filed for their benefits before or after their FRA (Full Retirement Age).

The simplest scenario would be if the deceased spouse had filed for their Social Security benefit after reaching their Full Retirement Age, and the surviving spouse filed for their survivor benefit after reaching their Full Retirement Age as well. In this case, their benefit amount would be 100% of the earning spouse's PIA, plus any delayed retirement credits they became eligible for.

If the deceased spouse had filed for retirement benefits before reaching FRA and was receiving a reduced benefit at the time of death, the survivor benefit will also be reduced. In this case, if the surviving spouse applies for survivor benefits after reaching their own FRA, the maximum reduction is 17.5%, meaning the minimum survivor benefit will be 82.5% of the deceased spouse’s PIA.

In the reverse situation, where the deceased spouse filed for retirement benefits after FRA, but the surviving spouse files for benefits before reaching FRA, the survivor benefit will be reduced by up to 28.5% of the deceased spouse’s PIA. This occurs if the surviving spouse files for survivor benefits at age 60, the earliest age they can apply.

Here is a simplified chart view of how the different scenarios will affect your survivors benefit.

How The Government Pension Offset Came Into Play

Now that we understand how spousal and survivor benefits are calculated, let’s revisit the overarching topic of the Government Pension Offset (GPO). As we mentioned earlier, the GPO significantly reduced, if not eliminated, the Social Security survivor and spousal benefits many retirees were eligible for. Let’s dive into a couple of examples to see how this played out for many people.

Let’s say Sally worked as a Connecticut public school teacher for 25 years and today is collecting a pension benefit of $2,760 per month. Sally’s husband worked over 10 years (40 quarters) at a covered job, paying into Social Security. After all the calculations were completed, Sally’s total spousal benefit should be $1,725.

However, because Sally has a Connecticut pension of $2,760, the total spousal benefit she can receive is limited to the amount that exceeds 2/3 of her pension amount ($1,840). In this case, Sally would not be eligible to collect any of the Social Security spousal benefit she would have otherwise been entitled to.

Now let’s look at an example of a survivor’s benefit, which can more significantly impact the financial security of a surviving spouse who can no longer rely on the Social Security benefit their spouse was collecting, nor the spousal benefit they were entitled to due to the 2/3 rule set by the GPO.

Let’s say John worked 35 years in covered employment, paying into Social Security, and his total monthly Social Security benefit was $2,875. John’s wife, Maria, worked as a Connecticut school teacher and collects a non-covered pension of $3,450. For this example, let’s assume John passed away. Under normal conditions, Maria would be eligible for the full $3,450 (adjusted for the time of retirement, as discussed above). For simplicity, let’s assume both spouses retired exactly at their FRA, so her survivor benefit would have been $2,875.

Due to the GPO, Maria would not be able to collect her full $2,875 survivor benefit from Social Security. She would only be able to collect any benefit exceeding 2/3 of her pension amount. So, 2/3 of her $3,450 pension = $2,300.

$2,875 (SS benefit) - $2,300 (2/3 pension) = $575 monthly benefit.

GPO Must Go

With the repeal of the GPO Maria, from our previous example, would now be eligible to collect her full survivor benefit, totaling an additional $1,425 per month! When we put the numbers on paper, it’s clear to see how significant this legislative change is for some families. For some households, the repeal will only result in a few hundred dollars more each month, but for many others, it could make the difference of thousands in monthly retirement income. This change was also enacted retroactively to January 2024. Meaning that any lost spousal or survivor benefits from that date will be calculated and paid in a lump sum to the affected parties. It is very important to log in to your Social Security Account and file for your benefit, if you haven’t already. I’m aware many people had an understanding that they weren’t going to be entitled to a benefit, so they may have never went through the process of filing. It is unclear how that instance will impact your benefit, if at all, or the timeline to have them restored fully if you do not have a registered account/have you benefits claim previously submitted. So I urge you to set up your profile and get your claim submitted. You can visit My Social Security Account and get started on this part today!

In conclusion

I’m sure if you’ve made it this far through the article, you can see just how powerful these legislative changes are for current and future retirees. The effects vary from individual to individual, some benefiting hundreds more in monthly retirement income, to others experiencing thousands in income now able to be realized due to the GPO repeal.

I am very happy to see this act having been passed and the expected relief it is bringing to my clients. As I mentioned before, it is unclear exactly how long it will take for full benefits to be restored, as the SSA has to recalculate and process payments for the millions affected by these two laws. However, they have signaled that it will take approximately a year, maybe longer, to have everyone’s benefits brought current with the new laws.

If you have a question or topic you’d like considered for a future episode/blog post, you can request it by going to www.retirewithryan.com and clicking on "Ask a Question."

As always, have a great day, a better week, and I look forward to connecting with you in the next blog post, podcast, YouTube video, or wherever we have the pleasure of connecting!

Written by Ryan Morrissey CFP®, CLU®, CHFC®, CMFC

Founder & Principal Wealth Advisor of Morrissey Wealth Management

Host of the Retire with Ryan Podcast